Profit and Loss Statement (P&L) - PART 1

.png)

A profit and loss statement (P&L) presents a company's earnings and expenses over a specific period. In other words, the income statement summarizes your revenues and subtracts your expenses to determine whether you netted profitably or ended with a loss. Net income or loss is also often referred to as the "bottom line." Your bottom line is a quick way to determine whether your company is moneymaking.

Single-step vs. Multi-step Statement

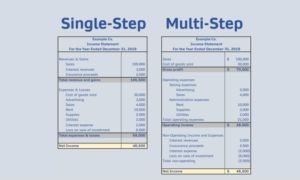

A single-step and multi-step statement are two ways to present a profit & loss. A single-step statement takes all revenues and gains and subtracts them from all expenses and losses. It allows you to see your ultimate bottom line in a single calculation. A multi-step statement differs as it first reports revenues and expenses to get to a total operating income. It then separately reports the gains and losses or nonoperating revenue/expenses. A multi-step statement is beneficial as it helps a company see its operating profit (loss) with one glance.[caption id="attachment_4171" align="alignnone" width="683"]

Single-step vs. Multi-step Statement[/caption]

Operating Income

Operating income is how much the company generates from doing what it does as a business. For example, how much profit does a pharmacy generate after selling its inventory and covering its overhead? Consider the scenario where the delivery truck had a total loss, and the insurance paid them $20,000. The 20 grand is income, but not operating income. It is a one-time occurrence and will be misleading to include it as part of the ordinary profit calculations. Fortunately, QuickBooks supports a multi-step income statement.

Profit ≠ Cash

An income statement reflects revenues when earned and expenses when incurred. By using this method of accounting, sales show up on your income statement even if sold on account. On-account sales are transactions that are not cash yet - they are sitting in your accounts receivable account. The same is true with expenses. Expenses show up on your income statement even if they were not paid in cash yet, e.g., when an insurance bill is received, it will be recorded as an expense. Awareness that the "bottom line" is not synonymous with "cash in the bank" will help business owners from making flawed decisions.

Reviewing a Profit & Loss

Several cardinal things to look out for when reviewing your income statement:

- Check your gross profit. While you may focus on looking at your "bottom line," your gross profit is also significant. Gross profit is net sales less any direct costs, referred to as the cost of goods sold (COGS). Gross profit tells you how much from your revenue is available after covering all your COGS, and how much can you afford your general expenses to be and still reach a profit?

- What is your bottom line? Is it positive (net income) or negative (net loss)? If it is a positive number, what can you attribute to the profitability? If it is negative, was your gross profit positive? Were your expenses too high?

- Where is the majority of your income coming from? Hopefully, the mainstream of your income is generated from operating revenue and not from one-time gains or nonoperating income.

- How do your expenses make sense to your overall firm? If you have loans, do you record the interest expense? Rent expense is a fixed expense, while office supplies are variable. Do you have a one-time expense in this period?

- Compare your numbers. Just because you netted positive in July of 2022 doesn't mean that the company was as profitable as it was in July of 2021. Watch the trend to make your numbers more meaningful.

Key Ratios

Two ratios that require income statement figures only:

- Gross profit margin. Gross profit margin is a percentage of sales dollars left after subtracting the COGS from the net sales figure. It measures the % of sales dollars remaining to pay the general expenses of the business. A gross profit margin of 29.2% means that for every $1.00 in sales, 29.2 cents is available to cover overhead and provide a profit.

- Net profit margin. The net operating profit is a percentage of sales dollars left after deducting all direct and overhead expenses from the net sales figure. This ratio measures what your return on sales was. If your net profit rate is 8.33%, it means that for every $1.00 in sales, the business is making a net profit of 8.33 cents.

Remember that these and other ratios are only as good as their comparisons. Follow the monthly trends or compare to other similar businesses.